Introduction

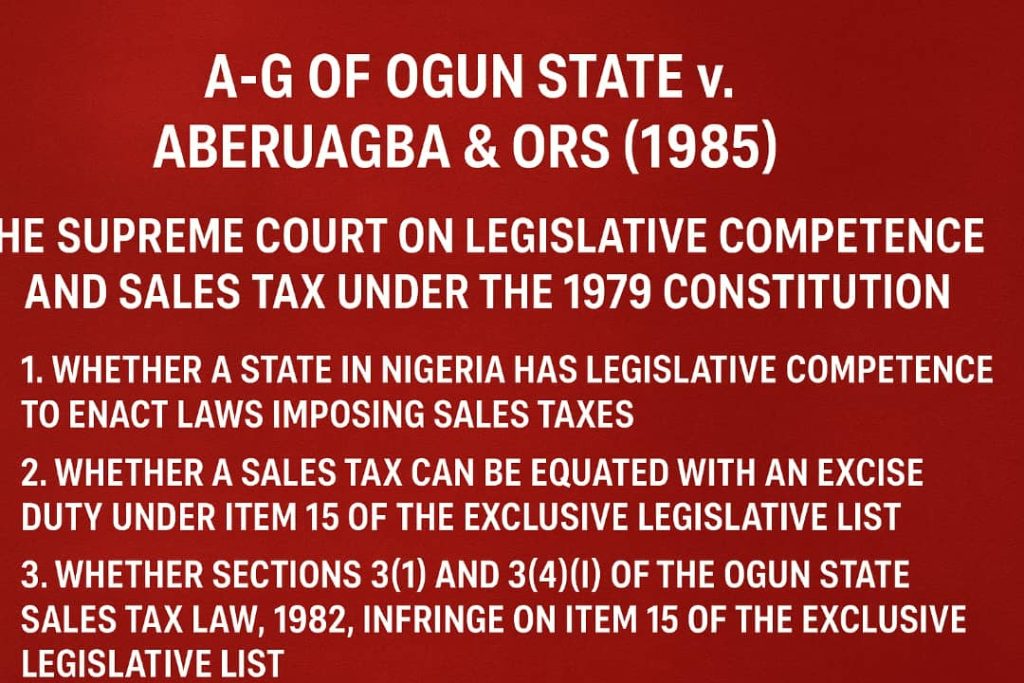

The case of Attorney-General of Ogun State v. Alhaja A. Aberuagba & Ors (1985) 1 NWLR (Pt. 3) 395 remains one of the most intellectually engaging constitutional law decisions in Nigeria’s judicial history. The Supreme Court, in this case, had to determine whether a State House of Assembly had the legislative competence to enact a Sales Tax Law that imposed tax obligations on certain goods and services within the State — particularly when such goods were brought from outside Ogun State or manufactured domestically.

This case stands as a defining judicial interpretation of Items 15 and 61 of the Exclusive Legislative List and the extent of State power under the 1979 Constitution. It raised questions about federal supremacy, interstate commerce, and the constitutional division of taxing powers between the Federal and State Governments.

Background of the Case A-G of Ogun State v. Aberuagba & Ors (1985)

The Ogun State House of Assembly enacted the Sales Tax Law, 1982,a statute that sought to impose a tax on the purchase of specific goods and services within the State. The law was designed to cover petroleum products, alcoholic beverages, tobacco, paints, and other specified commodities.

The central provisions under challenge were Sections 3(1) and 3(4) of the Law, which provided that sales tax was payable by the purchaser at the time of entering into the contract with the wholesaler. Importantly, the law required the wholesaler to collect and remit the tax to the State’s tax board.

The respondents challenged the law, arguing that it infringed on the exclusive legislative competence of the National Assembly, especially as it related to:

.Item 15 (Customs and Excise Duties)

.Item 61 (Trade and Commerce) of the Exclusive Legislative List.

The matter came before the High Court of Ogun State,which referred the constitutional questions to the Court of Appeal and ultimately to the Supreme Court.

Issues for Determination A-G of Ogun State v. Aberuagba & Ors (1985)

1.Whether a State in Nigeria has legislative competence to enact laws imposing sales taxes.

2.Whether a sales tax can be equated with an excise duty under Item 15 of the Exclusive Legislative List.

3.Whether Sections 3(1) and 3(4)(i) of the Ogun State Sales Tax Law, 1982, infringe on Item 15 of the Exclusive Legislative List.

4.Whether the phrase “and in particular” in Item 61 of the Exclusive Legislative List serves as words of emphasis or limitation in defining the scope of federal power over trade and commerce.

Decision of the Court A-G of Ogun State v. Aberuagba & Ors (1985):

Delivering the lead judgment,Nnamani, J.S.C., with whom the majority concurred, held that the Ogun State Sales Tax Law was partly unconstitutional as it encroached on the Exclusive Legislative List, specifically Items 15 and 61 of the 1979 Constitution.

On the Meaning of Excise Duty

The Supreme Court undertook a detailed exploration of the meaning of excise duty as used in Item 15. The Court examined several dictionary definitions and comparative authorities from Australia and Canada but warned against adopting definitions inconsistent with Nigeria’s economic context.

“Ordinarily, excise is the duty imposed on goods manufactured at home. It signifies a duty charged on home goods either in the process of their manufacture or before their sale to the home consumer.”

The Court agreed that a tax loses its character as an excise once it reaches the point of sale to the ultimate consumer. However, since the Ogun State Law imposed tax between wholesaler and retailer, it retained the characteristics of an excise duty.

On Legislative Competence of the State

The Court held that while States have power under the Concurrent Legislative List (Item H18) to regulate trade and commerce within the State, such power is limited by the Exclusive List and the inconsistency rule under Section 4(5) of the Constitution.

“That the Ogun State House of Assembly had power to legislate to impose sales tax on consumption of goods is beyond question, but the tax as framed under section 3(4)(i) of the Law is excise duty and is beyond the legislative competence of that Assembly.”

On Discrimination Against Interstate Trade

The phrase “taxable products brought into the State” in Section 3(1) of the Sales Tax Law rendered the law discriminatory, as it targeted goods brought into Ogun State from other States or abroad, without imposing equivalent tax on goods produced within Ogun State.

“Section 3(1) of the Law is equally bad as being discriminatory since as framed, no equivalent tax is imposed on goods manufactured or produced in Ogun State. The tax is only imposed on goods brought into Ogun State from other States of the Federation which ultimately will bear higher prices by the time they get to the ultimate consumer.”

Such discrimination, the Court held, infringed on interstate trade and commerce, which is the exclusive preserve of the National Assembly under Item 61(a).

On the Phrase “And in Particular”

The Supreme Court gave a landmark interpretation to the phrase “and in particular” used in Item 61 of the Exclusive Legislative List, holding that it was a phrase of limitation, not expansion.

“The words ‘and in particular’ in Item 61 of the Exclusive Legislative List are words of limitation. The exclusive power of the Federal Government under Item 61 to legislate on ‘trade and commerce’ is therefore limited to the matters specified in sub-items (a)–(f) and not intended to cover all aspects and ramifications of trade and commerce.”

This interpretation significantly preserved State powers over local trade and markets within their boundaries.

On Price Control

The Court further observed that the Federal Government, through the Price Control Act No. 1 of 1977, had already exercised its power under Item 61(e) to control prices of essential commodities. Since the goods listed under Ogun State’s Sales Tax Law (such as petroleum products, beer, and tobacco) were already regulated under the federal law, any attempt by the State to impose additional taxes thereon amounted to a constitutional conflict of legislative competence.

Key Dicta Established

“It would not accord with the economic realities of our country to give the term ‘excise’ an unduly restrictive definition.” – Nnamani, J.S.C.

“The tax will only cease to have the character of excise at the point when the goods are sold to the ultimate consumer.” – Nnamani, J.S.C.

“The words ‘and in particular’ in Item 61 of the Exclusive Legislative List are words of limitation, not of emphasis.” – Bello, J.S.C.

“Section 3(1) of the Law is discriminatory since it imposes tax only on goods brought into the State from other parts of the Federation.” – Supreme Court of Nigeria

The A-G of Ogun State v. Aberuagba decision remains a leading authority on constitutional law as concern fiscal federalism and legislative competence in Nigeria. It clarified the constitutional boundaries between federal and state taxing powers, emphasized the non-discriminatory nature of interstate commerce, and cemented the judicial view that state laws must not conflict with federal control over excise duties and price regulation.

The case also continues to guide discussions on tax harmonization, internal trade regulation, and the extent of state autonomy within Nigeria’s federal system.

A.G-OF BENDEL STATE v. A.G-FEDERATION & 18 Ors(1983) FULL SUMMARY

AFRICAN PRESS LTD V. THE QUEEN (1952) WACA 57–Sedition in Nigerian Law